A rather common method of hedging earnings or value at risk is entering into an interest rate swap transaction. As we get closer to a rising rate environment, some of you may question if using interest rate swaps to hedge make sense for your institution. Note that most major economic forecasts don’t have rates moving for at least another 12 months, which is what they said 12 months ago. So we continue to wait for the inevitable, however eventually you or someone in your ALCO committee may wonder exactly what an interest rate swap would do for you. Good news is that the Foresight model has the capability to do this type of What-If modeling! Learning the mechanics of setting the model up to do this can be seen and heard in a How-To video that we’ve recorded. Click here to see a listing of our How-To Videos. (You must have a FARIN Support Contract to view the How To Videos)

The following is an example of some analysis done on an institution to see what the results would be IF they entered into a swap transaction. Note that this analysis doesn’t include the cost to the broker or any other operational costs to enter the transaction. The example may be rudimentary to some however the objective of this post is mainly to be thought provoking to the reader and make them fully aware that this type of modeling can be done in Foresight.

Does Sample Bank need to hedge this commercial loan with an interest rate swap?

Sample Bank ($400MM Assets) has a successful commercial lender who recently was asked to quote a client on a $4MM commercial real estate loan. The loan pricing committee met and decided that they would quote the client 120 month balloon, 240 amortizing at 4.58% fixed. But how would this affect the position of the bank when related to their interest rate risk (IRR)? In other words, would putting this longer term fixed rate loan damage our IRR position? Would an interest rate swap hedge any perceived risk or would entering into a swap not make sense for the institution at this time? Sample Bank decided to get a quote on an interest rate swap to hedge this loan. On a notional amount of $4MM with 240 amortization Sample Bank would pay 4.58% fixed and receive 1 Mo Libor + 200 bps floating. At first glace, from an earnings perspective, this transaction is underwater when compared to the current rate environment. 1 Mo Libor + 200 bps is currently 2.15%, however as rates rise (if and when) the interest received increases. How quickly and when rates rise will determine if this transaction is “profitable” or reduces their IRR. Sample Bank decided to run two scenarios from their Foresight model: 1) Book the loan with NO swap 2) Book the loan WITH the swap. So they got everything setup in the model and ran the following analysis:

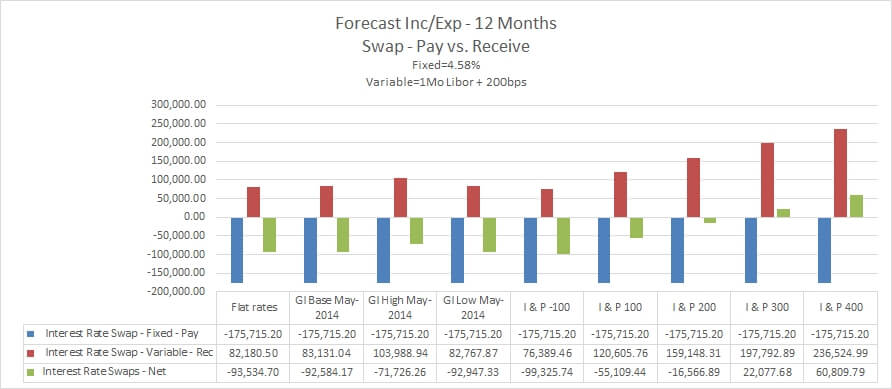

Earnings at risk

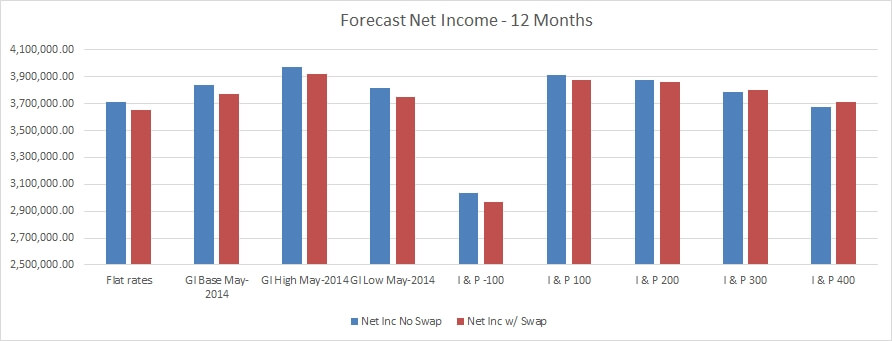

First they were able to isolate the earnings produced by the swap transaction over a twelve month period in various rate environments. The interest rate swap didn’t produce a positive income stream until the +300 rate shock environment. However we know that when rates increase more than 243 bps this transaction will be “profitable”. In the first twelve months or so rates don’t even rise enough in the Global Insight High rate forecast to produce a positive affect. When looking at both scenarios side by side it’s easy to see that the WITH swap transaction doesn’t produce more Net Income until the +300 rate environment. So from a short term earnings perspective it’s highly unlikely that this swap transaction will be of any use to the institution. (The report used in the model to produce these results is called the Forecast Income Statement Decision Matrix)